A Brief Look At Basic Commodities And The Lack Of Inflation

Commodity markets suggest deglobalization and supply shocks are the dominant force, not monetary inflation.

Rogue Macro | June 8, 2026

Macro systems are human systems. Rogue Macro explores the convergence of economics, biology, geography, politics, and demographics that shape the global economy.

With May CPI data coming out this week, economists are expecting another hot month, with the median forecast around 0.5%. Before we jump to conclusions, I wanted to take a look at some commodity charts and ask a simple question: do we actually have structurally higher prices?

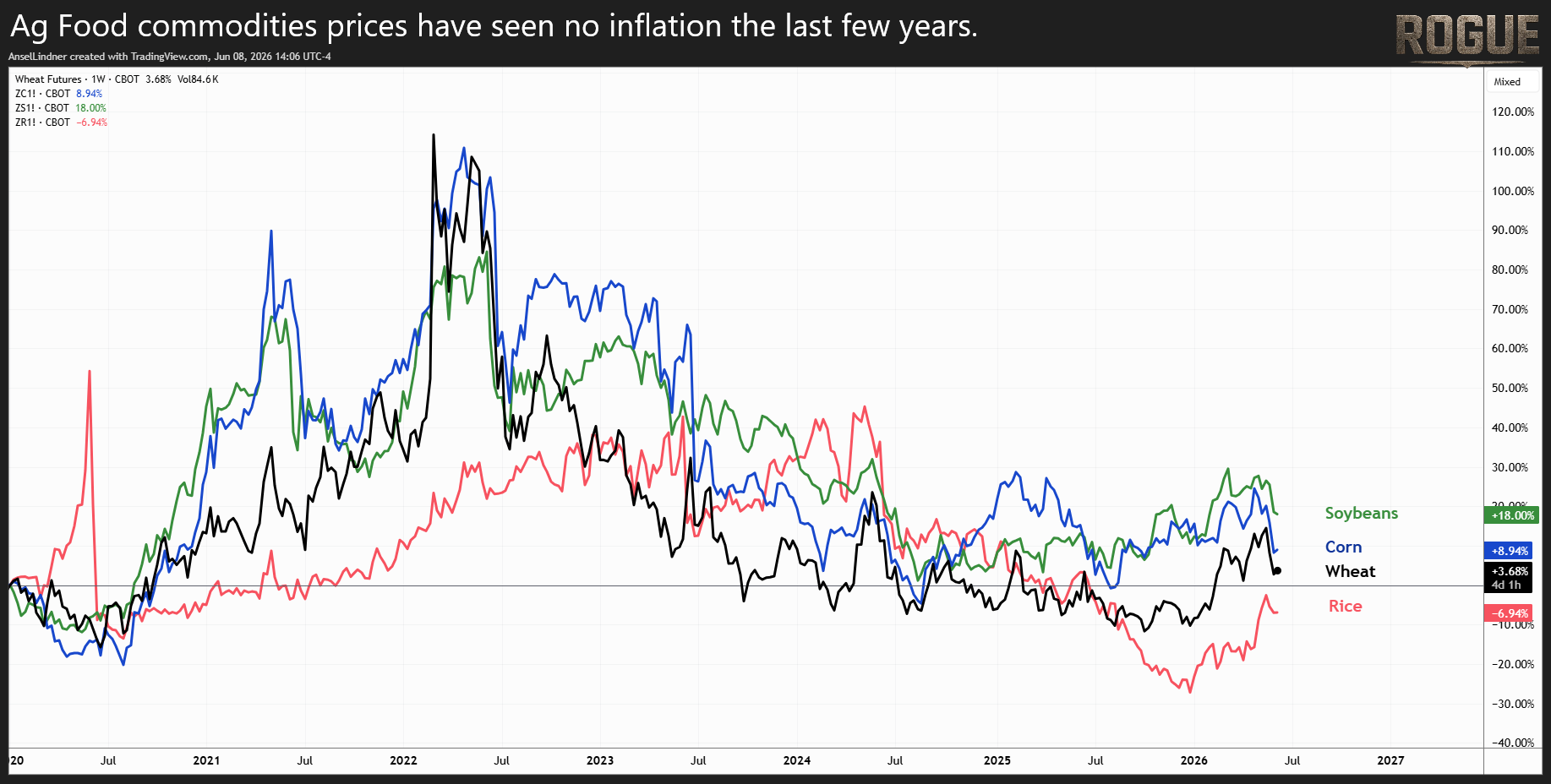

First up is grain. Below are wheat, soybeans, corn, and rice. In general, these commodities are flat to down over the last several years. The defining feature of the chart is the Russia-Ukraine War spike. Interestingly, prices began rising before the conflict officially started. Markets saw the troop buildup and understood there was a high probability that something significant was about to happen.

It didn't know the exact day, but it knew enough to start repricing grain months in advance. Compare that to today, where many commentators insist the oil market is somehow illogical or badly mispriced. I don’t think so.

More importantly, this price behavior does not match the popular money-printing explanation for inflation. We hear it constantly: "They're printing so much money." Fine. If that were the primary driver, then over a period of several years we should expect the most basic commodities in the economy to be rising. Wheat, corn, soybeans, and rice are among the foundational building blocks of the global economy. If the currency is being persistently debased, these are exactly the kinds of things that should be repricing higher.

The entire Russia-Ukraine spike has largely been unwound. Five years after the largest monetary and fiscal experiment in modern history, grain prices are flat to down. That is not what a structurally inflationary commodity market looks like.

What we are seeing instead is a world of bottlenecks, blockades, trade frictions, energy disruptions, and deglobalization. These forces can absolutely raise the prices of finished goods. They can make life more expensive. But that is not the same thing as a broad monetary inflation cycle pushing all real assets higher year after year.

In fact, this type of inflation is ultimately self-defeating. High prices damage demand. They slow economic activity. They encourage substitution and conservation. High prices are the cure for high prices.

This also fits my broader framework. Deglobalization and demographic decline are creating a slower, less efficient global economy. Every shock pushes us further in that direction. The result is periodic price spikes, weaker growth, and recurring recessionary pressures. This is not the 1970s, Kevin. It’s not an inflationary boom, it’s the push-pull grind lower.

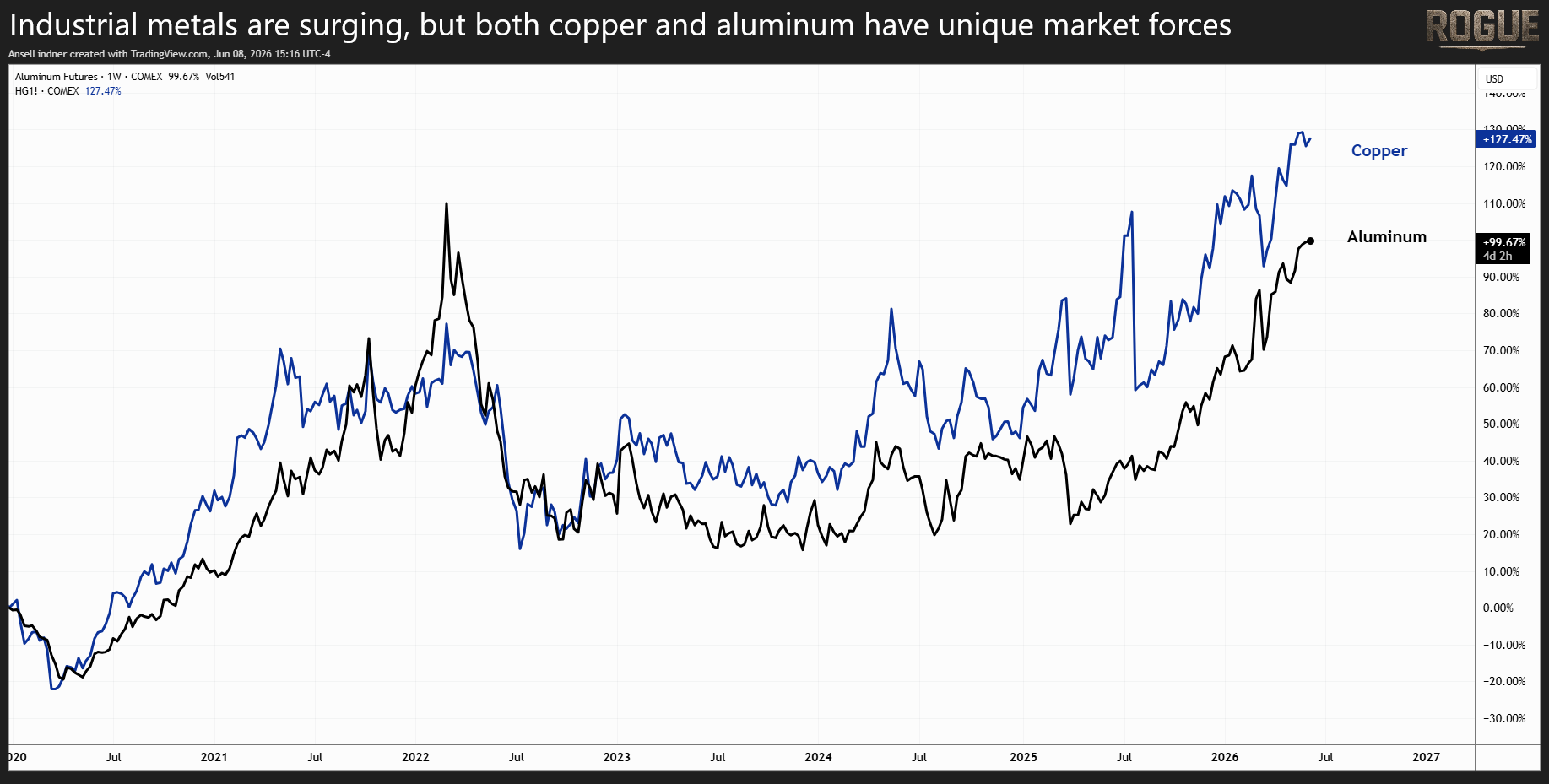

Of course, some commodities have risen. Copper and aluminum are two notable examples. Copper has benefited from the massive buildout of data centers and AI infrastructure. Aluminum appears to have greater exposure to energy markets and disruptions to global shipping routes. But isolated strength in a few commodities is very different from a broad commodity inflation cycle.

To summarize, CPI is running hot right now, but the commodity complex is telling a different story. This is not a money-printing story. It is a deglobalization story. And ultimately, it is a recessionary one.

ROGUE MACRO - Signal over noise. Predictive power over ideology.