Oil Shock or Not?

Is this the culmination of long-term trends or a financial overreaction?

Rogue Macro | Mar 9, 2026

Macro systems are human systems. Rogue Macro explores the convergence of economics, biology, geography, politics, and demographics that shape the global economy.

Welcome to my weekly “One Chart” posts. These public posts look at a single chart, or in this case, one asset across two timeframes.

The recent U.S. military operation involving Iran has spilled into the Strait of Hormuz. Many analysts long claimed the strait could never truly be “closed.” Yet, in practice, it effectively has been.

Not by decree from Iran, but by insurance markets.

After several tankers and civilian vessels were struck in the region, London marine insurers rapidly withdrew war-risk coverage. Shipping companies suddenly faced massive premium increases or no coverage at all. Even where policies could be renegotiated, many firms were reluctant to send vessels through the area.

The result was a sudden disruption to shipping flows and a violent speculative reaction in oil markets.

But that is exactly what this was: a speculative reaction, not a structural shift in oil fundamentals.

For years, many analysts have predicted a coming surge in oil prices due to Peak Oil or “Peak Cheap Oil.” When a spike like this occurs, they claim vindication. But those arguments were always about tight physical fundamentals driving prices higher.

That is not what happened here at all.

The current oil market is fundamentally characterized by oversupply. Major forecasting firms expected 2–4 million barrels per day of surplus production in 2026, likely flowing into inventories. This geopolitical episode may temporarily tighten flows, but it does not change the broader structural balance.

For oil prices to rise and remain elevated, the world needs strong economic growth. Military destruction doesn’t help, and we already know that deglobalization and demographic decline negatively affect baseline economic growth, and therefore oil demand.

At the same time, oil demand is famously inelastic, meaning consumption does not fall much when prices rise. People must commute to work, freight must move, aircraft must fly. Fuel consumption continues regardless of price. Instead, the adjustment happens elsewhere; fewer hires, less discretionary spending, and slower economic activity.

But demand is not perfectly inelastic.

Empirical estimates suggest that in the short run, oil demand elasticity ranges roughly between −0.03 and −0.10. That means a 10% increase in price reduces demand by only about 0.3–1%.

Over longer periods, demand becomes more flexible as consumers and industries adjust behavior, improve efficiency, or substitute fuels. Long-run elasticity estimates suggest a 10% price increase may reduce demand by roughly 3–8%.

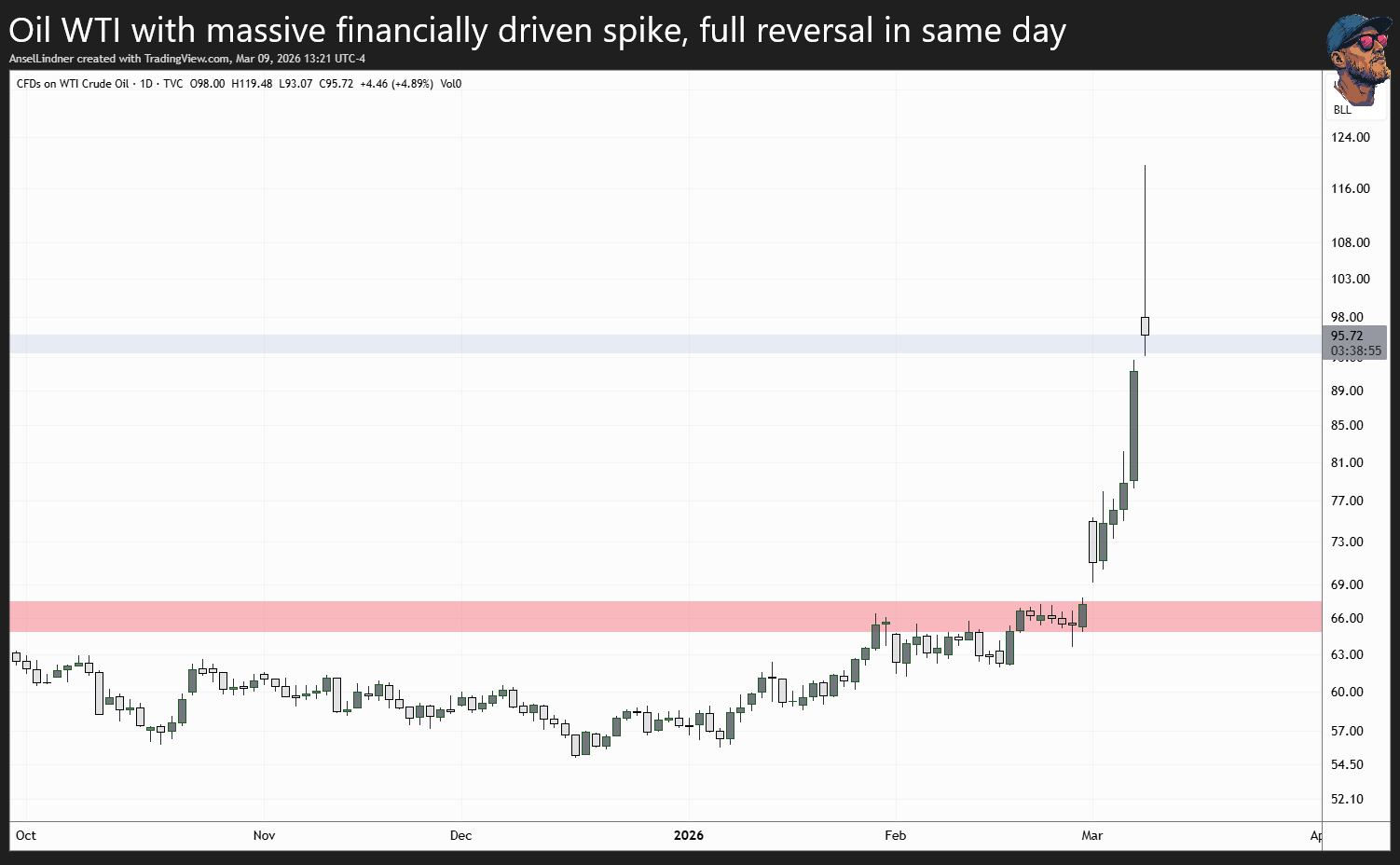

For now, the charts tell a simple story.

A geopolitical shock triggered a financial snap higher. Within hours, the market reversed.

This was a financial event, not the beginning of a structural oil bull market.

ROGUE MACRO - Signal over noise. Predictive power over ideology.

If you find this analysis useful, make sure to follow us everywhere!

Telegram community: https://t.me/+zBijvB3CxyA2OTYx

YouTube: https://youtube.com/@RogueMacro

Podcast (audio-only): https://podcasts.apple.com/us/podcast/rogue-macro-audio/id1882048839

or in your podcast app