The Reindustrialization Trade

Globalization led to financialization of the US economy, deglobalization promises to unwind that as the US reindustrializes.

Rogue Missive #126 | Feb 9, 2026

Financialization Was a Symptom, Not the Disease

For decades, the U.S. economy has shifted away from making things and toward finance. Wealth has increasingly been built through financial products and trading assets, not by producing physical goods. At the same time, manufacturing was pushed overseas in the name of efficiency. That choice wasn’t inevitable. It reflected a belief that globalization was worth the trade-offs, even if it meant weaker domestic industries, hollowed-out communities, and greater dependence on foreign production.

Many people saw this system as the inevitable outcome of a credit-based (fiat) monetary system. In that view, printing money to buy foreign products is just too tempting, your economy is hollowed out until something breaks and the system collapses.

That is the basic framing in much of macro today. To the mainstream and alternative financial press, it’s not a matter if but when the US economy collapses. Some focus on runaway inflation. Others focus on dedollarization and interest rates. Still others focus their analysis on growing ill will toward the United States and the rise of China.

These views share a common flaw: they ignore why globalization worked in the first place. Globalization was not a natural system grown out of a universal application of free market principles. To a degree that was a result, but it was a designed international order requiring non-market maintenance. A system like that does not need to collapse to unwind. It only needs a change in incentives.

Financialization was not primarily a monetary phenomenon. It was the natural outcome of U.S.-led globalization. The credit-based monetary system supported and extended that framework, but it did not create it. If money were the sole driver, and structural qualitative shifts are impossible, the doomers would be right. But globalization was the driver, and as the world moves toward deglobalization, the conditions that sustained financialization fade as well. Capital can rotate.

Subsidizing Globalization And Trade Accounting

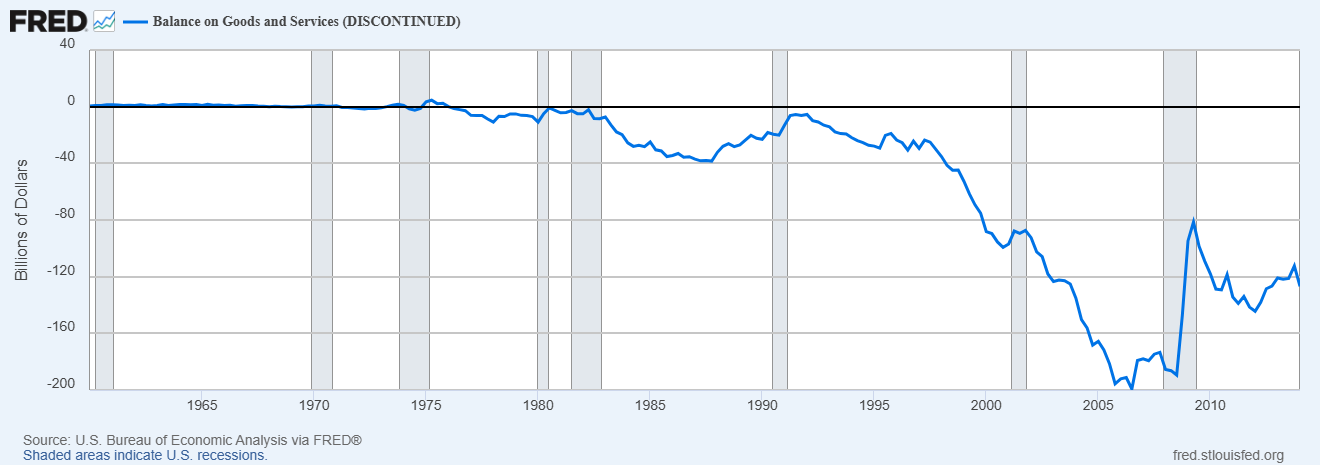

By the mid-1970s, the U.S. trade balance turned negative, and it has remained negative ever since. In nominal terms, the chart below shows the trade deficits of the 1980s associated with Japan’s export-driven rise, followed by far larger nominal deficits beginning in the late 1990s alongside China’s industrial expansion.

These persistent deficits were not the result of aggressive US trade policy. They were the consequence of a broader commitment to maintaining an open, rules-based global system. Other countries pursued growth through exports. The United States, in turn, upheld open markets and absorbed those exports. Domestic firms offshored manufacturing, while foreign producers competed directly for US consumers.

An economy’s output is composed of consumption, investment, government spending, and net exports. As globalization pushed net exports deeply negative and domestic industrial investment declined, other components naturally expanded to compensate. Consumption rose as a share of GDP, supported by credit and rising asset prices. Government spending grew to compensate for the resulting underemployment and costs for militarily maintaining the system. Everything become more financialized.

This is how the U.S. economy managed to grow steadily despite decades of trade deficits. Financialization could proceed as long as it didn’t grow too fast and introduce imbalances. The result was slow but stable growth.

Manufacturing-led economies tend to be volatile, with sharper cycles of boom and bust. Financialization-led growth, by contrast, is smoother but weaker. That smoothing reduced the frequency of recessions over time and allowed interest rates to drift lower year after year. No single catalyst drove this outcome. These patterns emerged naturally from the US role in sustaining globalization.

Image source: USAFacts.org

Financialization, in other words, was not an accident. It was a natural response to globalization, enabled by credit-based money, driven by incentives.

Rotation, Not Collapse

If financialization was a response to globalization, then the reverse may also be true.

As trade policy shifts, supply chains shorten, and geopolitical risk rises, the incentive structure changes. Capital no longer moves freely across borders in search of the lowest marginal cost. Resilience begins to matter more than efficiency. Domestic capacity becomes a strategic priority.

What’s often missed is what that rotation implies for the United States itself. For decades, developing nations enjoyed an industrialization process, building for the marginal global consumer, which happens to the US consumer. This pattern is very notable in the Japanese and Chinese “miracle” economies. Manufacturing investment, trade surpluses, and rising industrial capacity powered their ascent. The United States, by contrast, absorbed those exports and financialized instead.

Reindustrialization in the US reverses that role. The American consumer remains the marginal global consumer, but now the US is building its manufacturing base to serve them. As capital rotates back into domestic production, the US will now embody the rapid growth model of industrialization, driven by manufacturing investment, capacity expansion, and balance-of-trade improvement. In that sense, the United States becomes the next “miracle” economy through scale, energy abundance, and technological depth.

Phase One: The Energy Revolution

The first act of this rotation has already occurred. Reindustrialization began with energy.

Few realized just how geopolitically impactful the shale revolution was. The US went from the largest importer of energy, to being the largest producer and a net exporter. This shift unshackled the US from it’s role as guarantor in the global order. Where we once depended on it to secure our energy sources, we no longer do. The US is finally free to pursue its own interests.

Phase Two: AI, Compute, and Power

The second phase of rotation is now underway.

The AI boom is often framed as a purely digital phenomenon, but it is deeply physical. Data centers require massive power generation. Chips require fabs. Fabs require capital, materials, and skilled labor. Alongside AI infrastructure, investment is flowing into other strategic necessities: pharmaceuticals, rare earths, advanced materials, and other supply-chain bottlenecks for mandatory goods.

Where the first phase cut the chain requiring the US to subsidize globalization, this phase reflects a shift in priorities. Efficiency is no longer the sole objective. Reliability, control, redundancy, and national security now matter. Capital is being directed toward assets that secure domestic capability as we see clear in the AI capex boom.

This phase will still have speculative excess. The AI bubble has some more time to mature, but the important thing is to view it in the proper broader context of reindustrialization. The AI bubble won’t be the only one in the reindustrialization push. We could see a pharmaceutical or defense bubbles, too. We can’t be sure on the timeline, but this phase of reallocation toward strategic production is likely to take 10-20 years.

Phase Three: Broad Reindustrialization

The third phase will take the form of broad reindustrialization across the economy. It will extend beyond energy and strategic sectors into the unglamorous but essential backbone of production: tools, vehicles, machinery, and industrial components.

This shift will reshape the labor force and education as well. Many of these jobs will rely less on traditional four-year degrees and more on technical training, apprenticeships, and hands-on experience.

Positioning for the Reindustrialization Trade

If this framework is correct, portfolio construction has to change with it. Reindustrialization pulls an entire upstream and downstream ecosystem along with it, from raw materials, to energy, to transportation, to finished goods.

As production moves closer to home, commodities that were once treated as global, fungible, and easily sourced become strategic. Domestic mining, refining, and processing take on new importance because supply reliability and control matter more than finding the cheapest supplier halfway around the world.

In practical terms, this shifts attention toward:

Industrial metals: copper, steel, aluminum — the basic inputs for factories, infrastructure, and electrification

Energy inputs: production, refining, and transport — the fuel that makes industrial activity possible

Critical minerals: mining and refining for batteries, electronics, and defense systems

Construction materials: concrete, cement, and lumber — the physical foundation of new plants and infrastructure

Reindustrialization also changes how goods move. Shorter supply chains and domestic production increase demand for efficient internal transport rather than global shipping. Railroads, pipelines, and logistics infrastructure regain importance as the arteries of a production-based economy. We could finally see a rebirth of railroads in the US, as factories need mass transport of raw materials.

A full list of the top 20 assets and stocks to watch will be published for paid members in the next week. They will be my reindustrialization trade portfolio.

Please SHARE with others who might like it!

Follow on X @RogueMacro_

On Youtube